The digital advertising landscape in the Gulf Cooperation Council (GCC) is evolving rapidly, with the United Arab Emirates (UAE) and the Kingdom of Saudi Arabia (KSA) leading the way. Both markets exhibit strong digital growth, yet they have unique characteristics that set them apart. This article compares digital advertising trends in these two powerhouse economies, focusing on market size, industry contributions, advertising channels, mobile advertising, and regulatory dynamics.

1. Market Size & Growth

- UAE: Digital ad spending is projected to reach $1.709 billion by 2025, driven by high internet penetration and the increasing adoption of digital marketing strategies.

- KSA: The market is expected to grow from $1.15 billion in 2023 to $2 billion by 2032, with a Compound Annual Growth Rate (CAGR) of 5.80%.

Both markets are experiencing robust digital transformation, but KSA’s market is expanding at a faster pace due to increased government investments in digital infrastructure and the rise of local digital platforms.

2. Industry Contributions to Digital Advertising

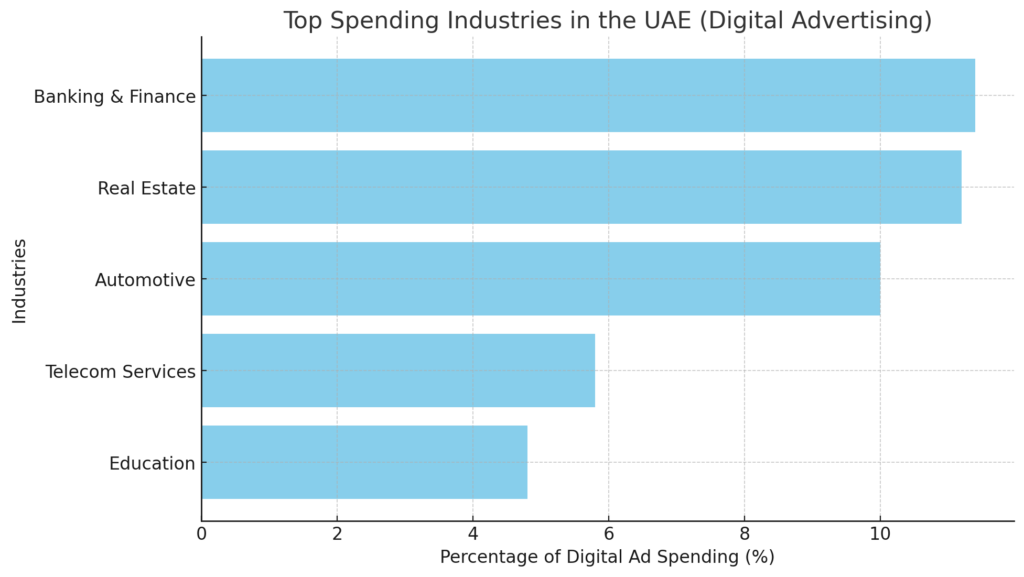

Top Spending Industries in the UAE:

- Banking & Finance (11.4%) – Leading due to competitive financial services and fintech adoption.

- Real Estate (11.2%) – Reflecting the UAE’s booming property market.

- Automotive (10.0%) – High demand for luxury and electric vehicles.

- Telecom Services (5.8%) – Driven by high smartphone penetration.

- Education (4.8%) – Strong digital presence in private and higher education sectors.

KSA’s Key Industries:

- While industry-specific digital ad spending percentages are less defined, major contributors include banking, real estate, and telecommunications. The entertainment sector, supported by Vision 2030, is also investing heavily in digital advertising.

- KSA’s increasing focus on local digital platforms is expected to shift more ad spend toward homegrown networks.

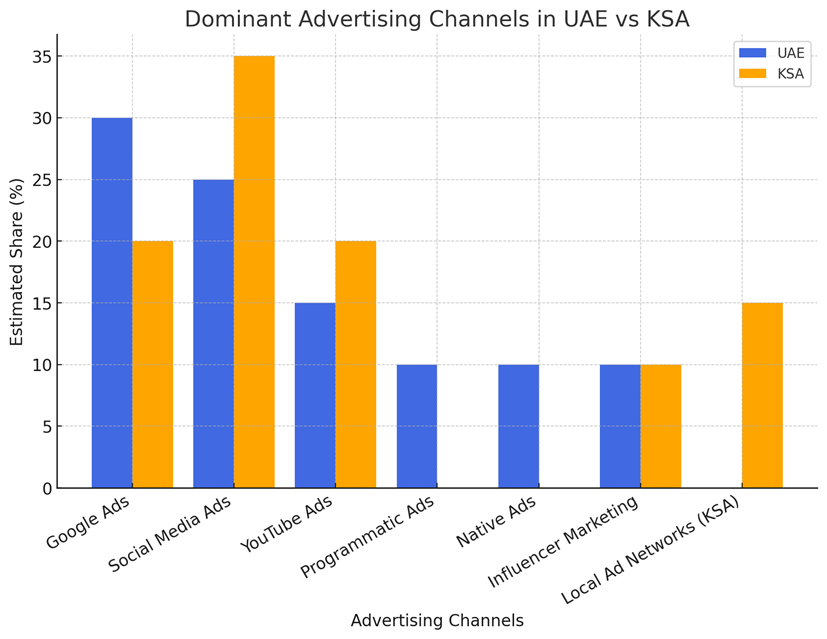

3. Dominant Advertising Channels

Both markets heavily utilize digital platforms, but their priorities differ:

UAE:

- Google Ads – Preferred for high-intent search advertising.

- Social Media Advertising (Facebook, Instagram) – Key for audience engagement.

- YouTube Advertising – Growing due to high video consumption rates.

- Programmatic Advertising – Automating ad placements for efficiency.

- Native Advertising – Seamlessly integrating branded content.

- Influencer Marketing – Effective for consumer engagement.

KSA:

- Social media advertising is the dominant channel, with projected ad spending exceeding $1.5 billion in 2024.

- Google Ads and video advertising are also strong contenders, with increasing reliance on mobile-first marketing.

- Government efforts are pushing for more local ad networks, reducing reliance on global platforms.

4. Mobile Advertising Growth

The mobile advertising market is expanding in both countries:

- UAE: Mobile ads are expected to represent 46% of total ad spending by 2028.

- KSA: Mobile advertising accounted for 28.1% of total digital ad spend in 2023, reflecting high smartphone penetration.

Both markets emphasize mobile-first strategies, ensuring businesses reach users on their preferred devices.

5. Regulatory Environment & Market Dynamics

- UAE: Digital advertising is regulated under strict data privacy laws, requiring businesses to comply with consumer protection guidelines.

- KSA: The government is focusing on keeping digital ad revenues within the country, supporting local digital platforms, and reducing reliance on foreign-owned advertising networks.

With KSA’s push toward economic self-sufficiency, businesses may need to adapt their digital strategies to align with national policies.

Key Marketing Takeaways

- For UAE: Marketers should continue investing in Google Ads, social media, and influencer marketing while optimizing for mobile experiences.

- For KSA: Brands should diversify digital spending between global platforms and emerging local advertising networks, aligning with government-backed initiatives.

Conclusion

The UAE and KSA are two of the most promising digital advertising markets in the GCC. While both share strong mobile penetration and digital transformation, KSA’s market is expanding at a faster rate due to government-driven digital initiatives. Understanding these differences can help businesses optimize their advertising strategies and stay competitive in both markets.

These sources provide valuable data and insights into the digital advertising landscapes of both UAE and KSA, covering market size, growth projections, industry contributions, and emerging trends in the region.

- https://www.grandviewresearch.com/horizon/outlook/digital-advertising-market/saudi-arabia5

- Provides data on Saudi Arabia’s digital advertising market growth and segmentation

- https://www.marknteladvisors.com/research-library/gcc-digital-advertising-market.html3

- Offers insights into the GCC Digital Advertising Market, including growth projections

- https://www.globenewswire.com/news-release/2024/05/28/2889205/0/en/Middle-East-and-North-Africa-Digital-Advertising-Market-to-Surpass-Valuation-of-USD-44-827-0-Million-by-2032-Astute-Analytica.html4

- Provides comprehensive data on the MENA digital advertising market, including UAE and KSA

- https://onaudience.com/programmatic-advertising-mena2

- Offers insights into programmatic advertising trends in the MENA region, including UAE

- https://www.sprinklr.com/blog/social-media-in-saudi-arabia/1

- Discusses social media trends and strategies in Saudi Arabia for 2025